By Derek Smith Jr

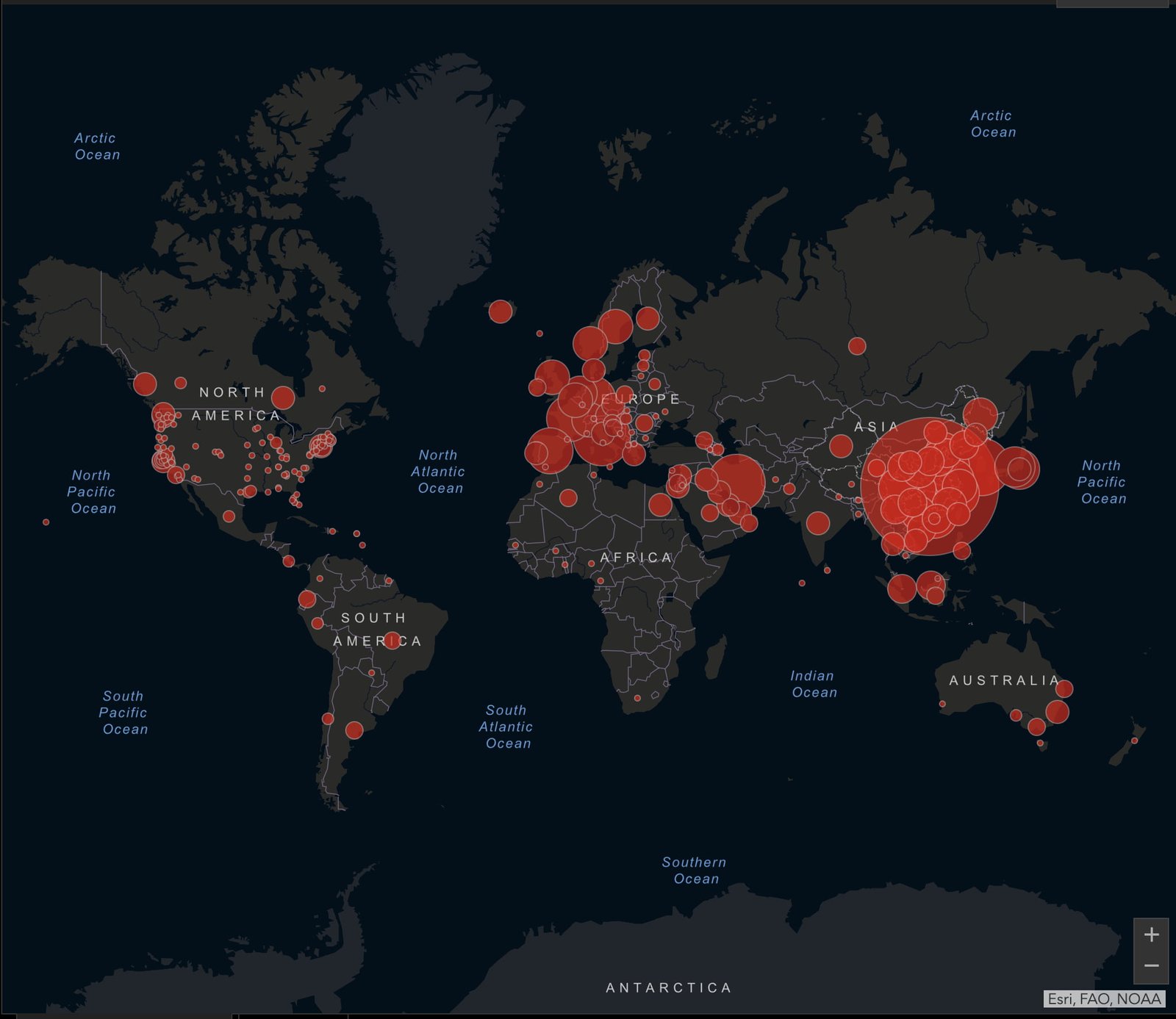

Life is about perspective and so is business. There were various public comments denouncing the European Commission’s release on May 7, 2020 where they essentially ‘blacklisted’ the Bahamas, yet again. What appears to have concerned both public officials and private enterprise is the European Union (EU) commission’s flagrant disregard for the impacts of the COVID-19 pandemic. Additionally, the pandemic has undoubtedly impeded the Financial Action Task Force’s (FATF) planned review of the Bahamas’ AML/CFT advancements. The FATF is relevant here because the Bahamas was in an ‘exit strategy’ that required a site visit by FATF, that has been delayed due to the pandemic yet the EU notes they are attempting ‘alignment with the latest FATF list’.

While I have strong views regarding the apparent bullying tactics used by the EU and their infringement on our sovereignty under the guise of an action plan for the comprehensive EU policy to prevent money laundering and terrorist financing, I would prefer risk and compliance professionals to shift their focus to ensuring their internal compliance and AML programs are robust.

As senior leadership navigate unprecedented economic and operational pressure, compliance professionals must simultaneously ensure that their compliance programs are strengthened during and after this pandemic.

A compliance program should be designed to adequately address the legislative environment of which the financial institution resides. Additionally, I believe there are several factors that distinguish an ‘average’ program from “robust” program.

Tone From The Top (Culture)

Culture is essentially the core of the risk and compliance environment. Scandals are potentially around every corner in today’s environment. Maureen Mohlenkamp, principal with Deloitte Advisory noted in a 2015 release, “Fundamentally, culture is about how things get done in an organization. The power of culture can be extraordinary.” Therefore, cultivating value-based approach is needed during this pandemic and after as it will reinforce principles of integrity and ethics while completing tasks.

Procedures & Training

Your suite of AML compliance policies and procedures is extremely important. Reviewing them during this pandemic to ensure they remain appropriate, agile, and adequate may be a good idea. Ensuring these documents are accessible to all employees and easy to follow will assist with adherence to them. Also, developing communication strategies surrounding policies and procures will help with employees’ familiarity with the information. Training can take the form of virtual session considering the social distancing environment. Also, compliance professionals must ensure that training are targeted for the various levels of your organization. Furthermore, training schedules should be designed for all facets of the institution.

Assessment Regime

The AML processes and procedures must at minimum meet the respective AML guidelines of the jurisdiction of which your entity does business. Your money laundering and terrorist financing assessment strategies will be pivotal when determine the potential risk to the institution and how the client should be treated throughout its relationship with your institution. Moreover, an adequately designed risk-based approach could lead to more efficient management of the onboarding process.

Chief Compliance Officer (CCO)

Sourcing for this position should not be taken lightly. A CCO must have a combination of skills inclusive of expert knowledge of the regulatory environment, compliance analysis tools and can demand respect at all levels of the organization. The individual selected is a powerful statement about the organization’s commitment to ethics and compliance. Moreover, their placement in the organizational structure sends positive or negative signals to the regulator regarding the tone at the top.

Testing and Monitoring

The COVID-19 pandemic has not halted the regulatory requirements to continuously monitor the risks associated with your business. Financial institutions should have independent evaluations and testing annually, and reports given to senior management and the audit committee on the buoyancy of the AML compliance program. Additionally, internal monitoring of reports and allow for self-identification on violations of AML laws which then allows for corrective action plans to be designed and commenced before the regulator arrives for their reviews.

This pandemic period — though disruptive in a myriad of unanticipated manners— can be considered an opportunity or a threat. I encourage my colleagues to think positively and reflect upon their compliance program both as it operates now and how it can adapt in future uncertain times.

{kind=link}